Money laundering affects an estimated 2–5% of global GDP each year, equivalent to a staggering $754 billion to $2 trillion. Detecting money laundering early is critical, as this financial crime can seriously damage your business operations and reputation. In the U.S. alone, involvement in money laundering can result in penalties of up to $250,000 and five years of imprisonment.

As criminals develop increasingly sophisticated methods, your anti-money laundering (AML) compliance strategy must keep pace. A well-designed AML monitoring system can help you spot suspicious behavior before it escalates. Equally important is understanding key AML risk factors, such as the use of real estate to move illicit funds or structuring deposits just below the $10,000 reporting threshold to avoid detection.

This expert guide outlines the essential steps to help you identify and prevent money laundering schemes that could harm your organization. From understanding how money laundering typically works in business environments to recognizing warning signs and implementing effective detection systems, you’ll learn practical strategies to protect your operations from this growing financial threat.

How Money Laundering Works in Business Settings

Money laundering typically follows a structured three-stage process designed to disguise the criminal origins of illicit funds. Understanding this cycle is essential if you want to prevent your business from being unknowingly used as a laundering vehicle.

Phase 1: Placement

The first stage is placement, where illegal funds are introduced into the legitimate financial system. This often involves breaking down large cash amounts into smaller transactions to avoid triggering suspicious activity reports or depositing them through cash-heavy businesses.

Phase 2: Layering

The second stage, layering, creates complexity by moving the funds through multiple accounts, companies, or even countries, making the money trail harder to trace.

Phase 3: Integration

Finally, during integration, the “cleaned” money is reintroduced to the economy as seemingly legitimate income, ready for use.

Cash-intensive businesses are prime targets for money launderingschemes. Restaurants, convenience stores, parking garages, and vending machine operators handle large amounts of cash daily, making it difficult to distinguish between lawful income and illicit deposits. Criminals often blend illegal cash with daily revenue to make it appear legitimate.

Trade-based money laundering (TBML) is another widespread tactic, responsible for an estimated $240–600 billion annually, according to the UN. It involves manipulating cross-border trade through under- or over-invoicing, multiple invoicing, or falsifying product descriptions to move illicit value undetected.

Shell companies—legal entities with no real operations—also play a major role in masking the true origin and ownership of funds. These entities help criminals conduct suspicious transactions with minimal scrutiny. High-risk industries such as real estate, precious metals, casinos, and financial services are especially vulnerable due to the high volume and value of transactions.

Ultimately, detecting money laundering means understanding these schemes and implementing AML monitoring systems tailored to your industry and risk exposure. Awareness of these patterns forms the foundation of a strong anti-money laundering defense.

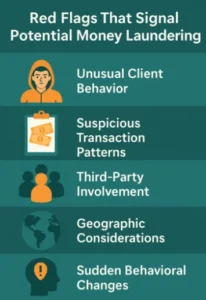

Red Flags That Signal Potential Money Laundering

Detecting suspicious activity requires vigilance and knowledge of specific warning signs. Recognizing these red flags enables you to identify potential money laundering schemes early and protect your business from criminal exploitation.

Unusual Client Behavior

Unusual client behavior often serves as the first indicator. Be wary of clients who seem unnecessarily secretive or reluctant to provide basic information about themselves, their business, or the source of their funds. Also, raise concerns when clients with no geographical connection to your location seek your services. Such secrecy might involve reluctance to disclose personal details or beneficial ownership information.

Suspicious Transaction Patterns

Suspicious transaction patterns are a major warning sign. Pay close attention to transactions that are unusually large, frequent, or inconsistent with the client’s profile or the nature of your services. Transactions involving unfamiliar jurisdictions or structured to stay below reporting thresholds—typically under $10,000—may be efforts to evade detection.

Third-Party Involvement

The unexplained involvement of third parties can signal layering activity. Be cautious when clients use third-party payments without a clear reason. These transactions often come from unexpected sources, making it harder to trace the origin of funds. In such cases, thorough documentation and scrutiny of the third party’s financial background become essential.

Geographic Considerations

Geographic risk plays a crucial role in identifying suspicious behavior. Transactions involving countries with weak AML regulations or those listed by the Financial Action Task Force (FATF) as high-risk should be examined with extra care, as these jurisdictions are often linked to financial crime and money laundering.

Sudden Behavioral Changes

Watch for sudden changes in transaction patterns or client instructions. Unexpected urgency, frequent modifications, or cancellations without a clear explanation could indicate an attempt to move funds quickly or confuse detection systems. These behaviors often precede suspicious or unlawful activity.

Consequently, implementing robust AML monitoring systems helps identify these warning signs before they escalate into serious compliance issues or reputational damage. Being proactive in spotting these red flags allows your business to stay ahead of potential financial crime.

How to Detect and Investigate Suspicious Activity

Implementing effective monitoring systems is the cornerstone of detecting money laundering before it harms your business. The most reliable approach combines automated transaction monitoring with skilled human analysis, allowing you to identify suspicious behavior early and accurately.

Transaction monitoring is typically the first line of defense. These systems automatically scan financial activity using predefined rules and risk scenarios. Advanced platforms support both real-time and batch monitoring and allow the creation of tailored scenarios for risks such as structuring or pass-through accounts. For best results, your monitoring should use dynamic thresholds based on customer risk profiles rather than applying a uniform set of rules across all accounts.

In many financial institutions, a Money Laundering Reporting Officer (MLRO) plays a central role in detection. This mandatory role involves analyzing suspicious transactions, overseeing AML compliance, and filing Suspicious Activity Reports (SARs) with authorities. The MLRO must have sufficient authority to report directly to financial intelligence units without needing prior approval.

In addition to transactional data, customer behavior analytics can enhance detection efforts by identifying deviations from established behavior patterns. This method builds customer profiles and compares them against historical data and peer group norms. Unlike rigid rule-based systems, this context-driven analysis reduces false positives and flags genuinely suspicious behavior more accurately.

For high-risk customers, implement Enhanced Due Diligence (EDD) measures such as:

- In-depth verification of identities and ownership structures

- Closer scrutiny of the source of funds

- More frequent and detailed transaction reviews

- Additional background checks, especially for politically exposed persons (PEPs)

Clear internal escalation procedures are also critical. Employees should know exactly how to report concerns to the MLRO or a designated officer. These internal channels support regulatory compliance and help prevent criminal liability under laws like the Proceeds of Crime Act.

Ultimately, the most effective AML defenses combine the speed and scale of AI with the contextual judgment of trained human analysts. While technology is essential for analyzing large datasets, human expertise is irreplaceable when it comes to interpreting complex behaviors and understanding nuances that automation may overlook.

Turning Insight Into Action

Detecting money laundering requires a proactive and well-informed approach that combines automated monitoring with human analysis. By understanding how laundering works, recognizing behavioral and transactional red flags, and implementing systems like dynamic thresholds, due diligence, and internal reporting channels, you can protect your business from severe legal and reputational risks. Effective AML strategies are not just about compliance—they’re a vital part of responsible business operations in a high-risk financial landscape.

Sources:

- https://www.semantic-visions.com/

- https://www.lawsociety.org.uk/topics/anti-money-laundering/money-laundering-warning-signs

- https://www.veriff.com/kyc/news/detecting-money-laundering-a-comprehensive-guide

How Accounting Firms Deliver Accuracy In Financial Reporting

How Certified Public Accountants Support Tax Planning Year Round

5 Reasons Business Accountants Are Critical For Startups